Quick summary

Selling your Bitcoin to cover expenses triggers capital gains taxes and locks you out of future growth. Discover how using Bitcoin as collateral for a low-interest loan allows you to access the cash you need today while maintaining 100% ownership of your assets.

If you’ve been in the Bitcoin space for more than one market cycle, you know the feeling. You’re sitting on a healthy stack of sats, watching the charts, and firmly believing in the long-term value of Bitcoin. But then real life happens. You need to buy a car, pay for a wedding, or cover an unexpected tax bill.

The traditional financial advice is simple: sell your assets to cover your costs.

For a Bitcoiner, however, selling is painful. It often means triggering a taxable event (capital gains), shrinking your stack, and potentially watching from the sidelines as the price rockets up immediately after you sell. This is the "HODLer’s Dilemma."

But there is a third option that wealthy investors have used for decades with stocks and real estate, and it is now available for your Bitcoin: Borrowing against your assets.

Here is why using your Bitcoin as collateral on Ready is often the superior financial move compared to selling it.

1. The Tax Advantage: Debt is Not Income

The biggest friction point in using Bitcoin for real-world expenses is taxation. In most jurisdictions (including the US, UK, and EU), swapping Bitcoin for fiat currency is a taxable event.

- Scenario A (Selling): You bought 1 BTC at $20,000. It is now worth $60,000. You sell $10,000 worth to pay for home renovations. You have realized a capital gain on that portion, meaning you now owe the taxman a percentage of that money. Your purchasing power just shrank.

- Scenario B (Borrowing): You pledge a portion of your Bitcoin as collateral to take out a stablecoin or fiat loan via Ready.co. Because you haven’t sold the asset, you have not triggered a capital gains tax event.

Note: Tax laws vary by jurisdiction, so always consult a tax professional. However, generally speaking, loan proceeds are not considered taxable income.

2. Opportunity Cost: staying in the Market

The history of Bitcoin is riddled with stories of people who sold early to buy something tangible - like the infamous "10,000 BTC for two pizzas." While you likely aren't buying pizza, selling Bitcoin to buy a car today could mean that the car effectively costs you ten times its value in future purchasing power.

When you borrow against your Bitcoin, you maintain 100% exposure to the market.

If Bitcoin appreciates while your loan is active, your collateral value increases. Once you pay back the loan principal and interest, you get your Bitcoin back—which may be worth significantly more than when you started.

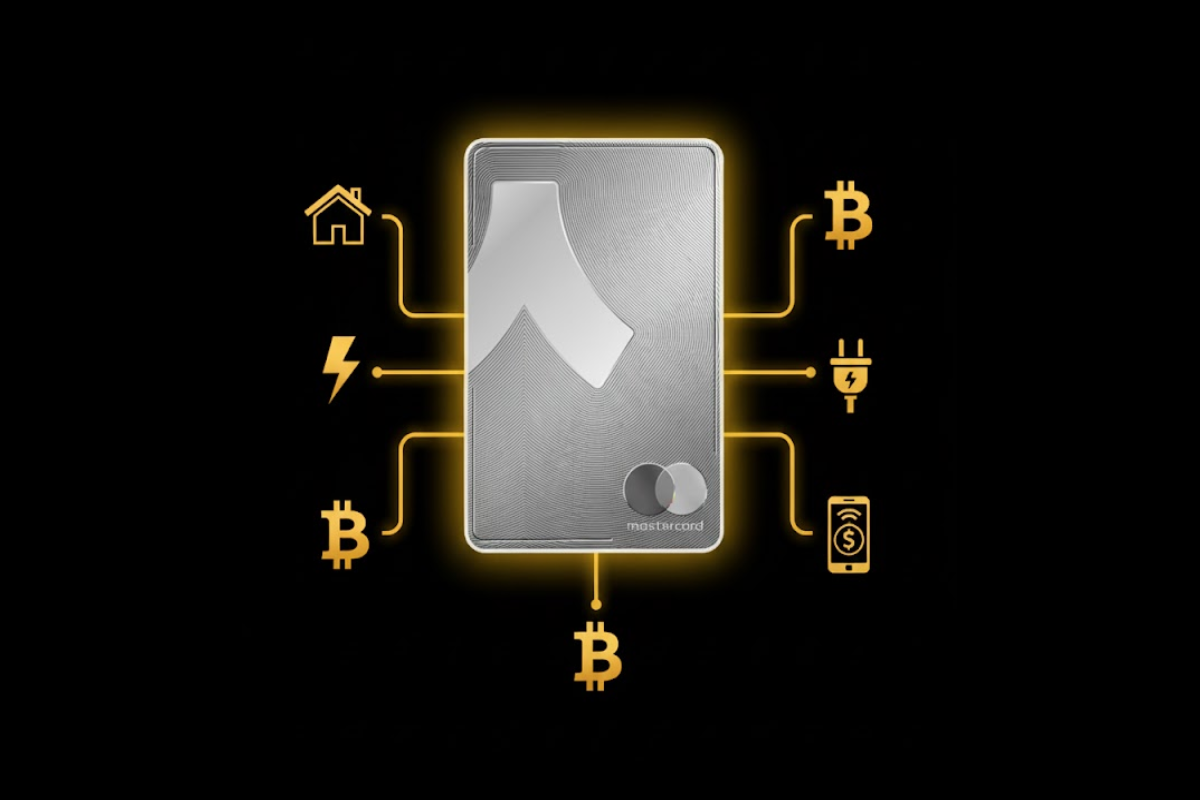

3. How It Works on Ready

We have streamlined the borrowing process to be as friction-free as the asset itself. Unlike a bank, we don’t need to see your credit score, pay stubs, or tax returns. Your Bitcoin is your creditworthiness.

- Download Ready: Available on iOS and Android

- Deposit Collateral: Deposit Bitcoin into Ready

- Set Your Terms: Choose your Loan-to-Value (LTV) ratio. A lower LTV (e.g., 20-30%) offers a higher safety margin against market volatility.

- Get Liquidity: Receive stablecoins (USDC) instantly.

- Spend: Spend those funds directly from your Ready card

Need more help? View the full guide here on how to borrow against your Bitcoin.

4. Managing the Risks (LTV and Margin Calls)

Borrowing is not without risk. If the price of Bitcoin drops significantly, the value of your collateral decreases. If it drops below a certain threshold, you may face a "margin call," where you must add more collateral or pay down part of the loan to avoid liquidation.

This is why conservative borrowing is key.

- Don't max out: Just because you can borrow 80% of your Bitcoin’s value doesn't mean you should.

- Keep a buffer: Sticking to a conservative LTV (like 30-50%) allows the Bitcoin price to fluctuate significantly without threatening your position.

The "Buy, Borrow, Die" Strategy for Everyone

Ideally, you never want to sell your hardest asset. By utilizing Ready’s borrowing features, you are effectively adopting the strategy of the ultra-wealthy: live off low-interest debt secured by appreciating assets.

You get the cash you need today, you keep the Bitcoin you’ll need tomorrow, and you keep the taxman at bay. That is financial sovereignty.

Get started

Ready to start borrowing? Download the Ready mobile app today.